Post War – 1946 to 1961

Post War – 1946 to 1961

War Ends - Peace Restored

World War II ended in Europe with Germany’s unconditional surrender on May 8, 1945, and in the Pacific with Japan’s surrender on August 15, 1945. Germany was divided into the Western and Eastern occupation zones, a denazification program was instituted, and Nazi war criminals were prosecuted. Germany gave up about one-fourth of its 1937 territory to the USSR and Poland. The United Nations was organized. Two independent states emerged from Germany - the Federal Republic of Germany and the German Democratic Republic. Rather promptly, Poland, Hungary, East Germany, Czechoslovakia, Romania, and Albania became Soviet satellite states.

Yugoslavia pursued an independent policy. The roots of the Cold War took hold. The U.S. occupied Japan, and Korea was divided North and South at the 38th parallel between Russia and the U.S. The Marshall Plan (1948-51) led to the “German economic miracle.” The economies of Italy and France rebounded favorably, that of England only modestly. Japan experienced substantial growth. China ended its civil war and its economy settled down. By 1952, the economies of a number of nations led by that of the U.S. were humming along at a very good clip.

Top Management Transition

On November 13, 1946, A. G. Becker’s Chairman, Robert Schaffner, who joined the firm at its inception in 1893, and who succeeded A. G. Becker as President upon his death in 1925, passed away at the age of 70 at Michael Reese Hospital after a long illness. He had been closely supported for some twenty years by David Stern as Vice President and then President. Stern, following Schaffner’s death, was elected Chairman of the Board. In 1947, James H. Becker, son of A. G., having been with the firm since 1921, was elected President.

Commitment to Equities: NYSE Membership

The post-WWII period started out with a short-term bear market, stocks declining some 24% from May 1946 through June 1949, reacting to a bull market rise between April 1942 and May 1946 of some 129%. However, mid-1949 through December 1961 was the 12-year period during which, as below described, Becker initiated a major strategic commitment to the equity securities business. That commitment was enhanced by a strong bull market rise of some 350%, or an average growth rate of some 11% compounded per annum (except for a short-term “hiccup” in late 1957). Short-term commercial paper rates generally but gradually moved up over this twelve-year period from about 1% to over 4%, reflecting a fairly steady and robust business expansion. Total market outstandings grew from some $400 million in the 1946-51 period to over $1.9 billion in 1963.

The firm also benefited from fresh leadership provided by the David Stern/James Becker duo.

In July 1947, symbolic of the firm’s commitment to and prospects for equity research, underwriting, and the marketing of common stocks, the firm organized an affiliated general partnership which became a member of the New York Stock Exchange. At the time, this arrangement was required by Exchange rules. Shareholders and general partners of these sister entities were the same, and they were: David Stern, James Becker, Moses Shire, Lester Roth, Francis Patton, Vladamar Johnston, Howell Murray, Andrew Baird, Irving Sherman, Joe Levin, Henry Getz, Harry McCosh, Raymond Egger, and Carl Stern. Irv Sherman became the general partnership's representative member of the New York Exchange.

A financial statement of A. G. Becker & Co., Incorporated, published for October 24, 1947, showed total footings of $3.7 million and a net worth of $2.4 million. As of the same date, the affiliated general partnership, A. G. Becker & Co., the NYSE member firm, showed footings of $472 thousand and a net worth of $206 thousand. About one year later, the respective financial statements suggested aggregate net income being earned for the period of between $150 and $200 thousand. In a Tribune article in March 1952, A. G. Becker’s capital was reported to be just under $3.2 million.

As of January 1, 1949, Francis Patton retired and William Mabie, Herbert Schaffner, Maurice Cann, Alwin Pearson, Charlie Ritter, David Dattelbaum, and Russell Boyd were brought into the A. G. Becker general partnership as partners and into the corporation as shareholders. With Francis Patton's retirement, the number of partners/shareholders was 20. During the same year, Elmer Hassman joined the corporation as a Vice President heading the Municipal Bond Department, later bringing in Wally Hintz.

The archives do not have a copy of the shareholder agreement in effect in early 1949, but it may be assumed that David Stern and James Becker had significant percentage interests in the common stock of the firm and that the other 18 shareholders shared roughly equally in the balance of the common stock ownership. It may also be assumed that the 17 new shareholders (excluding Moses Shire), in aggregate, provided the firm with a substantial amount of new capital which helped to offset the redemption of Robert Schaffner’s interest.

In 1953, the NYSE changed its policy to permit corporate memberships. With this, the Becker partnership was liquidated and the affiliated corporation took over the firm’s NYSE seat, continuing to be personally represented by Irv Sherman. The shareholders of the corporation had not changed from the earlier list for 1947 which was supplemented as of January 1, 1948.

In December 1949, the Chicago, Cleveland, St. Louis, and Minneapolis-St. Paul Stock Exchanges combined to form the Midwest Stock Exchange, headquartered in Chicago. With this merger, David Skall joined Becker as a specialist and odd lot dealer on the MSE, moving to Chicago from Cleveland. Dave became a General Partner of the firm in 1950. Malcolm (Mac) Skall, Dave's son, joined his father on the MSE in 1952. Sadly, Lester Roth passed away in that year, and with this event, the number of shareholders returned to 20.

In June 1952, the Tribune paid tribute to Chairman David Stern for his fiftieth anniversary at A. G. Becker & Co., noting his directorships of Gillette, Cummins Engine, and John Morrell, as well as his honorary Trusteeship of the University of Chicago from which he graduated in 1902. Mr. Stern retired in 1954, leaving the post of Chairman vacant at that time.

Fresh Emphasis on Securities and Corporate Analysis

As noted earlier, the firm initiated an “analytical” or “statistical” department shortly after A. G. Becker’s death in 1925. The early work of this department, as best can be determined, was short-term credit analysis related to commercial paper issuers, and long-term credit evaluations related to preferred stocks, intermediate-term notes, and bonds. These tasks, under Robert Schaffner and David Friday’s guidance, also included some “macro” evaluations, especially as to the general European - and more particularly German - and South American economic conditions.

Due Diligence

In the mid-to-late 1930s, whatever junior staff existed in this department, under the oversight of Joe Levin and then later Harold “Woodie” Wood, began to provide the financial analytical dimension of “due diligence” as required under the recently legislated 1933 Securities Act. As the firm began to do more common stock underwritings in the late 1930s and into the 1940s and 1950s, and started maintaining trading and inventories in such securities and providing information to investors, true “investment research” and "due diligence" became a necessity. At the same time, these efforts provided an opportunity to generate business and achieve competitive differentiation. In light of his greater responsibilities, “Woodie” Wood, who joined the firm in 1929, was elected a Vice President in 1953 and became a shareholder in 1957.

As part of the "due diligence" process, in parallel to the need to undertake a financial analysis of an issuer of securities of which a firm was the managing underwriter, it was equally important that the manager participate in the drafting of the registration document and the prospectus to be provided potential investors. This "disclosure" work was initially overseen by Levin but in due course was transferred to Kent Sykes. Like Woodie, Kent joined Becker in 1929, having previously been in the newspaper and advertising business. As such, Kent also took over Joe Levin's supervision of the firm's advertising. By 1950, Woodie and Kent were very much working closely together.

Investment Research

With the membership on the NYSE in 1947, investment research of common stocks became a sine qua non. To address this need, Don Gally, formerly a vice president and investment officer with the Central Trust Company (Cincinnati), was hired to head the “new” department as of January 1, 1948. It is not clear how or whether the department prospered under Gally, and what happened to him. In May 1952, John J. Fox was hired to succeed Gally as head of the "Analytical Department" in Chicago and remained its head until late 1954. During the short tenure of Gally and Fox, the work of Clarence (“Gus”) Torrey was overseen. Gus joined Becker in 1950 (coming from a small local Chicago investment house) and became a “senior analyst,” specializing in the oil industry.

It was also during this period (late 1940s, early 1950s) that the firm opened, and shortly afterward closed, an office in Cincinnati.

Growth of Institutional Investing

As noted earlier, institutional investing activity was growing rapidly. Investment research by securities firms was increasingly being directed to and valued by professional portfolio managers, analysts, and trading desk personnel in mutual funds, insurance companies, and pension fund managers. Firms providing excellent research were rewarded with commissions on trading executions or on commissions "given up" by other stock exchange members who were executing trades and receiving NYSE fixed commissions. A preponderance of these growing investment institutions were located in the major Eastern cities - New York, Hartford, Boston, Philadelphia - and the analysts and salesmen servicing them were primarily on Wall Street. Becker had few if any analysts in its New York office at this time and needed to build that capability from scratch. To that end, Jim Becker, with the assistance of Vince Flett, hired Lawrence Kahn in early 1955 as Vice President in charge of investment research to be located in the New York office (and with oversight of the small Chicago department). Larry was formerly the manager of E. F. Hutton’s research department. Shortly after joining Becker, Larry was elected Treasurer of the New York Society of Security Analysts, and a few years later, President, which roles gave him a good vantage point from which to build an investment research team and program. More about that program later.

Block Trading

In the post-war years, institutional investors, and in particular mutual and pension funds, experienced great growth. By reason of their size, many funds would have substantial positions in common stocks which, to accumulate or to liquidate on the New York Exchange in the normal course of hundred-share transactions, would take long periods of time and have great uncertainty as to the average price realized on a large position. Out of this situation developed the “cross” and “positioning” role of a number of brokers including Becker. The trading desks at many mutual fund sponsors and other institutional fund managers developed relationships with their counterparts at selected brokerage firms - people in whom they had trust and who by reason of their specialization and/or the firm’s investment research following in certain securities, they could “open up” with and discuss their overall position goals with respect to a particular security, to be achieved via an accumulation or a liquidation. The agent firm would then selectively scout the institutional market, tentatively arranging a trade or set of trades to purchase or sell, as applicable, large “blocks” of the specific security, being prepared to inventory a long or short position as might be necessary to complete the total trade, all on the basis of an agreed upon price among the parties involved. The total potential “trade,” when all agreed, would then be “taken down” to the NYSE floor and “crossed” typically after some minor changes for the specialist as principal and agent to “clear his book.” This “block trading” activity had its genesis in the 1950s especially under the leadership of Goldman Sachs and Bear Stearns, but Becker was an active participant as well, especially through the work and talent of Harry Weber in the New York Office and Herb Schaffner and Maury Cann in Chicago, with their close ties to the top investment officers and traders at certain major mutual funds, supported by exceptionally talented trading desk personnel both in Becker’s New York and Chicago offices.

Investment Banking

Underwriting and Distribution

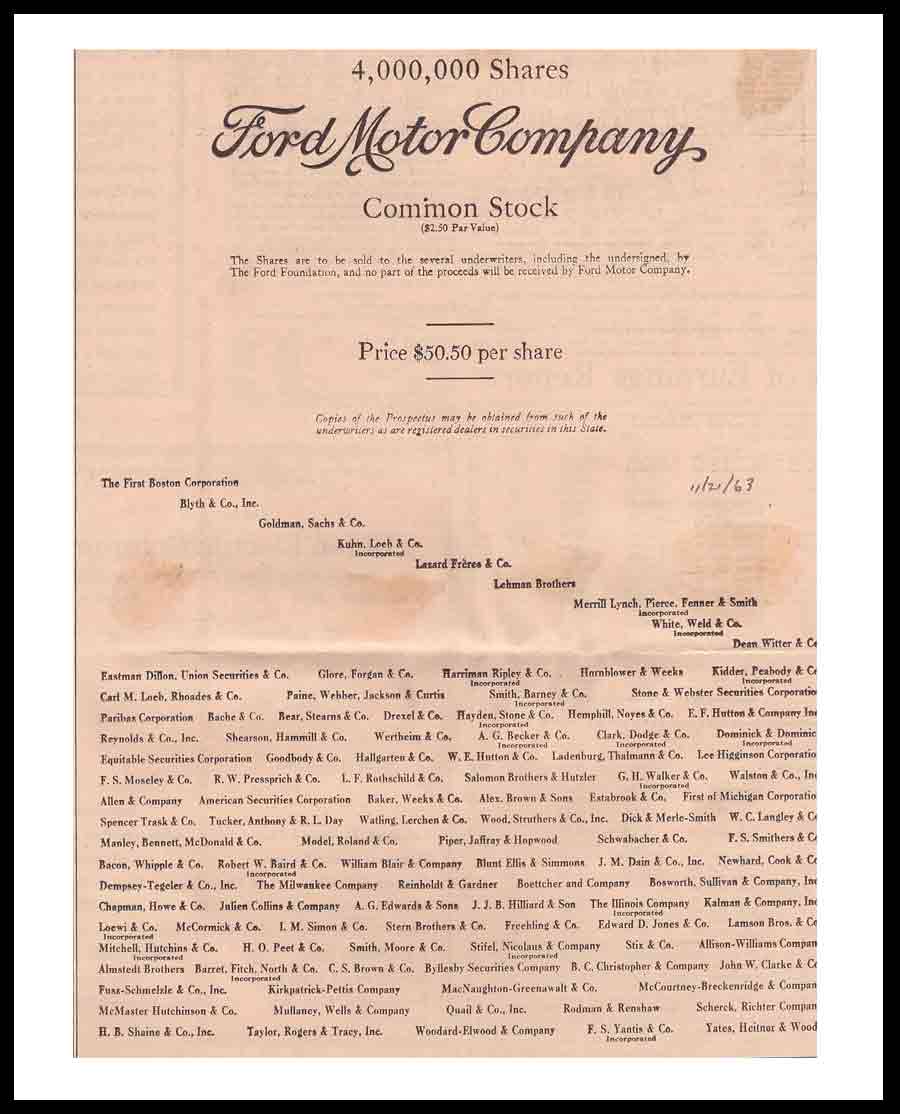

All during the postwar period and continuing into the 1950s, and then on into the 1960s, the underwriting and distribution of public offerings of corporate and municipal bonds, equipment trusts, and corporate preferred and common stocks was a central activity within A. G. Becker & Co. The firm was recognized “on the street” as a reliable, trustworthy, financially sound, and competent “sub-major” underwriter and distributor of offerings of all categories by the then leading old-line Wall Street “houses of origination,” such as Morgan Stanley; Kuhn, Loeb; Dillon Read; Blyth; and First Boston. The structure of underwriting syndicates followed some clear protocols as reflected, for example, in the “tombstones” of two major offerings in 1962 and 1963. As noted Becker was a sub-major at this stage of the firm's development.

{kind=link}

{kind=link}

In many cases, by reason of strong relationships with chief executive and corporate finance officers, Becker was able to obtain "major" underwriting positions, and in some cases, "special bracket" treatment. Halsey, Stuart & Co., a Chicago-based bond house, had for many years organized syndicates to make bids for the competitively offered bond issues of public utilities and railroad companies. Halsey, over the years, was quite successful in competing with the major New York houses. Becker was a regular mainstay participant taking major positions in these Halsey-led syndicates.

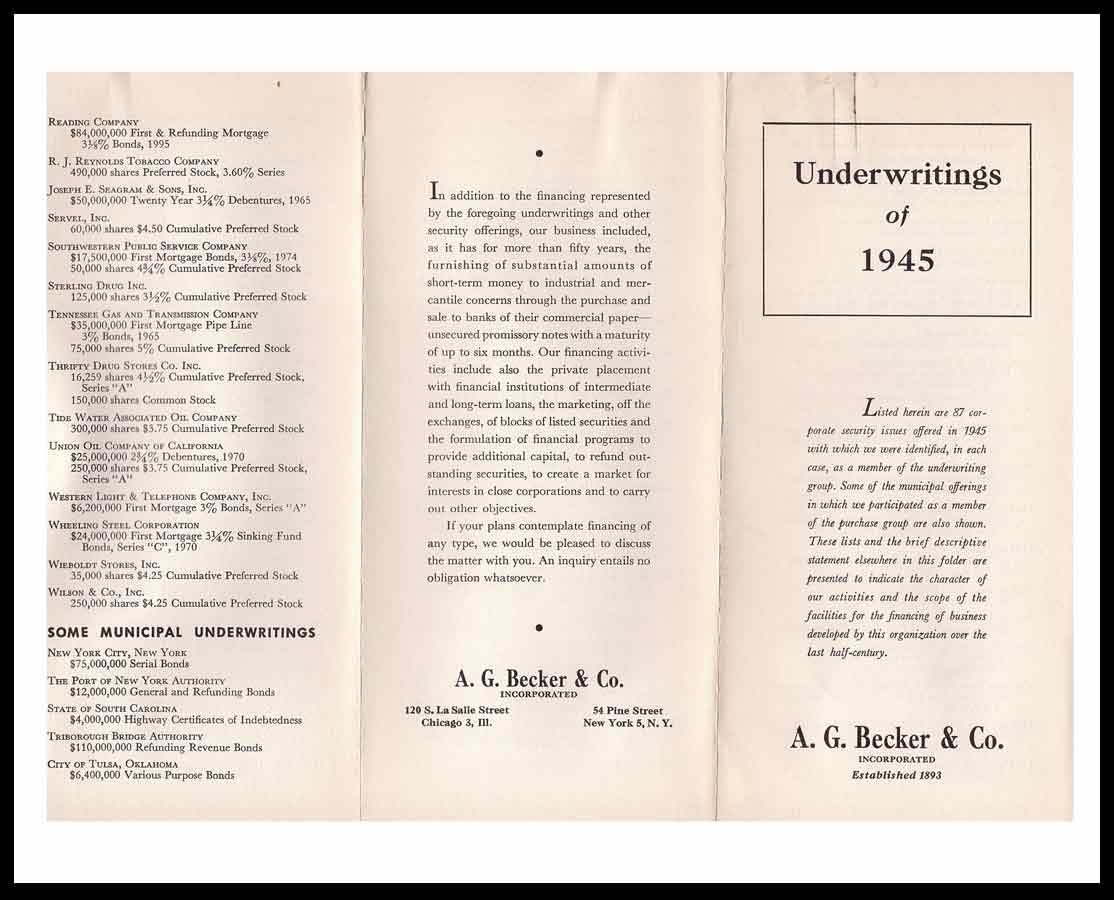

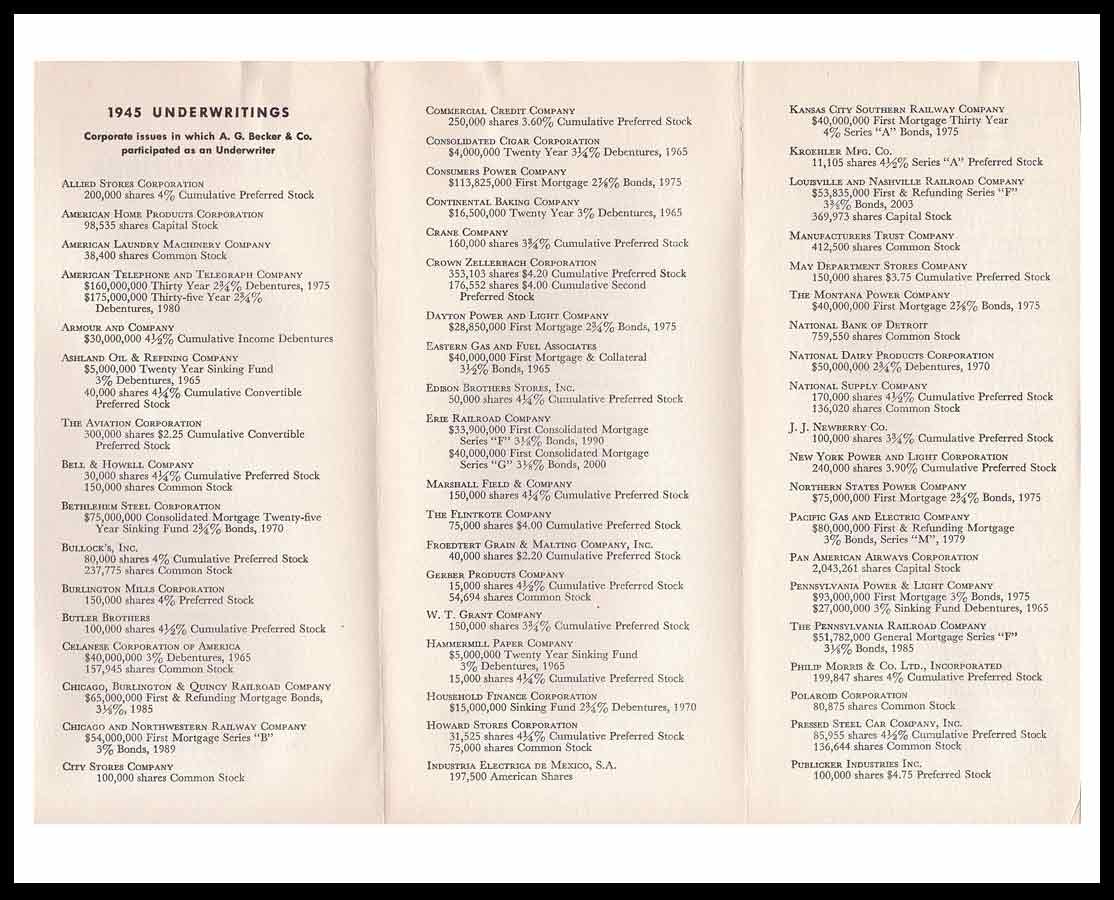

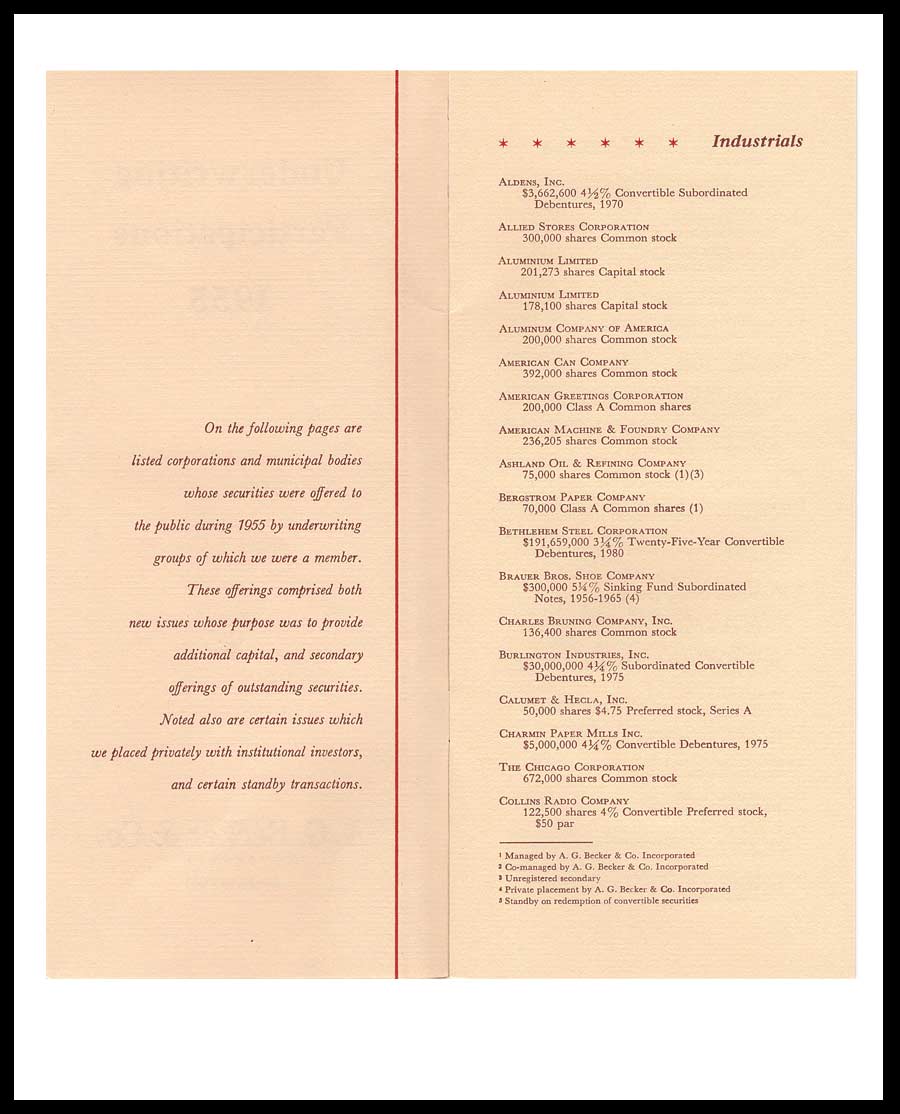

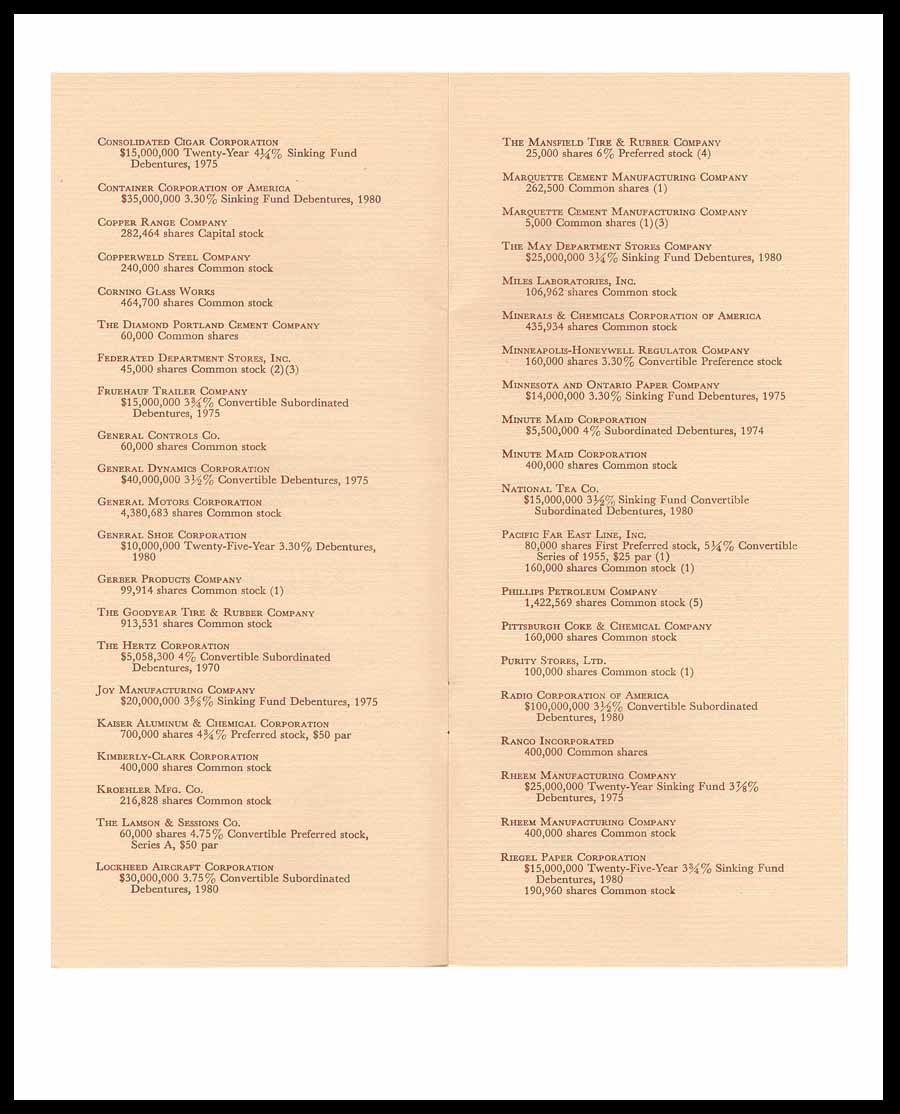

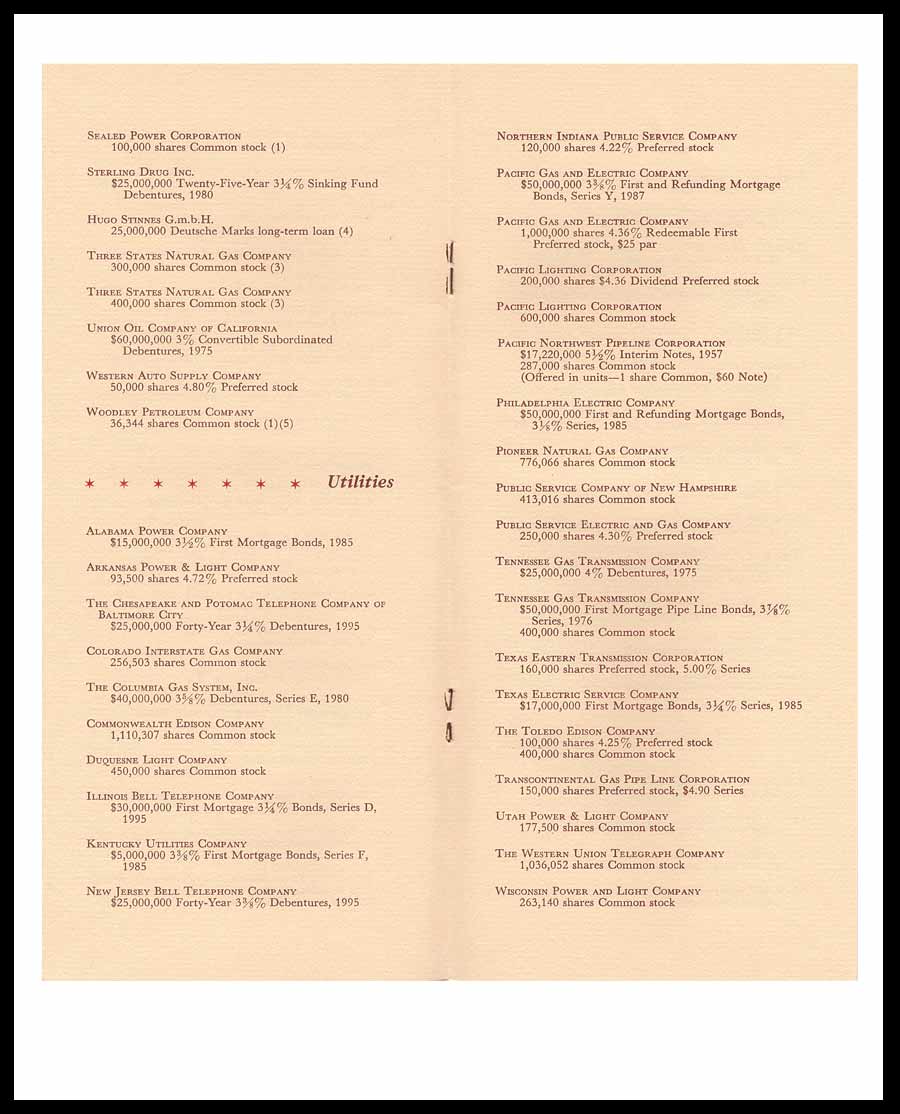

On balance, however, from 1945 until the 1970s, when Becker began clearly to be a “house of origination,” and, in parallel, began to display relatively powerful fixed-income and institutional equity distribution abilities, the firm was pleased to be a “participating” underwriter, and to have steady access to underwrite and market most of the new issues of the day. The Newberry Archives have copies of letters which at year end James Becker regularly wrote to the heads of the major underwriting firms thanking them for inviting Becker into their deals during the year just completed. He received very nice responses. Regularly, the firm enclosed, in early year mailings to clients, a listing of the underwritings and securities handled during the year (1945A, 1945B, 1955A, 1955B, 1955C, 1955D, and 1955E). Notice the difference in the length of the list for 1955 vs 1945. In many ways, the emphasis on dealing in underwritten securities harkened back to the days of A. G. Becker when he promoted the provenance of underwritten investment securities.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Becker’s standing in the underwriting syndication world was maintained in good part on the firm’s strong distribution capabilities in fixed-income securities and institutional equities, and to its traditional distribution of common stocks in the Midwest. However, the firm’s position also rested in part on the foundation of industry relationships established by Francis Patton in the 1930s, followed by the consistent and persistent efforts of Andrew Baird into the 1960s. Andy, through his extensive involvement in the IBA, NYSE, NASD, MSE, and Chicago Bond Club, expanded on Fran Patton’s work by establishing relationships with a new generation of industry leaders. He was given operational support through the day-to-day syndicate communications of Art Curtis in the Chicago office, who was elected a Vice President in 1952. The need for similar efforts and leadership in the syndication function in the New York office would not be addressed for some years.

Corporate Finance Transactions

During the period of 1946 to 1961, the firm continued to extend its corporate finance services and relationships to old and new clients through public financings, private placements, and distributions of blocks of stock for “old” clients - in many cases, through multiple transactions. These clients included such diverse businesses as Gardner-Denver; Cummins Engine; Acme Steel; Visking; Heyden Chemical; Ashland Oil; Mead Johnson; Abbott Labs; Kentucky Utilities; Younker Brothers; Cook Coffee; Holeproof Hosiery; City Stores; Mansfield Tire; Marquette Cement; Hines Lumber; Woodley Petroleum; Gerber Products; Parker Pen; Federated Department Stores; Hammermill Paper; International Cellucotton; Quaker State Oil; Howard Stores; Katz Drug; Hooker Chemical; Nunn Bush; and Universal-Cyclops Steel.

Public offerings, private placements, and other corporate finance services were rendered to new clients in the period 1946-1961, including such companies as Purity Stores; Hammond Organ; Great Northern Oil; American Potash; Minnesota Pipe Line; Michigan Gas; City Ice and Fuel; City Products; Briggs & Stratton; Ohrbach’s; Lytton’s; Carson Pirie; Chicago, Rock Island & Pacific; Ketay Instrument; Sealed Power; Bergstrom Paper; Danly Machine; Murphy Corporation; Amurex Oil; Lit Brothers; Rhinelander Paper; St. Regis Paper; Larsen Company; Natural Gas Distributors; Pacific Far East Line; Dyson Corporation; Spector Freight; Jostens; Wolverine Shoe; Premier Industrial; Detroit Foods; Crawford Corporation; Packard Instrument; Dean Milk; Inland Life; R. D. Irwin; AMT Corporation; Deltown Foods; Creative Playthings; Acceptance Finance; and Franklin Finance.

The private placement of longer-term (10-20 year) debt instruments with major insurance companies came into vogue in the 1950s and expanded substantially in the 1960s and forward. Perhaps the initiator of this development was the Prudential Life Insurance Company which began to decentralize its investment activities by authorizing the purchase of privately placed debt by its regional offices. The company also began to consider smaller loans extended to smaller enterprises, where yields could make up for the added administrative costs and risks. Other major insurance companies - and then those of lesser size - followed this practice and began to have personnel specializing in privately negotiated debentures, including in due course subordinated debt, with carefully negotiated, restrictive covenants.

Becker caught onto this trend fairly early and privately placed the debt of Lit Brothers and Lytton’s in 1950, and followed later with the private placement of bonds and preferred stock for Michigan Gas and Electric, as well as Nunn Bush. If memory serves, a large private placement of the Notes of Universal-Cyclops Steel was completed during this period with the Prudential home office and handled by Jim Becker himself. As described below, this was the foundation for Becker’s active private placement debt activities in the 1960s and forward.

In 1947, the firm represented the Toni Company and its shareholders (brothers Irving and Niesen Harris) in the sale of Toni to Gillette. This transaction reportedly was the investment banking industry’s first deal in which the proceeds the sellers received varied upwardly geared to the earnings of the Toni division over a period of years after the acquisition - a so-called “earn-out” deal.

As earlier noted, A. G. Becker & Co. was instrumental in the 1929 creation of Fashion Park Associates (through Jim Becker); the 1930 merger of Auto Strop into Gillette (through David Stern; and the just described 1947 sale of Toni to Gillette (through a team of David Stern, Jim Becker, and Irv Sherman). Throughout the U.S. economy during this period, the consolidation of businesses picked up substantially. Commensurately, the role of investment banker in these transactions began to grow. Becker participated in this trend by negotiating a number of deals including Howard Stores’ acquisition of Foreman & Clark; American Radiator’s acquisition of Detroit Controls; St. Regis Paper’s acquisition of Rhinelander Paper and, later, of St. Paul and Tacoma Lumber; Minnesota Mining and Manufacturing’s acquisition of Zenith Plastics; Aetna Industrial’s acquisition of Eisendrath Glove; Younker Brothers’ acquisition of T. S. Martin; Dyson Corporation’s purchase of Waukesha Motors; and Genesco’s acquisition of Formfit.

Organizational Development

Vince Flett

Perhaps the most significant addition to the organization in this period was James Becker’s recruitment of Harvey Vincent Flett in early 1953. Vince, a Canadian born in Nova Scotia in 1907, immigrated to the U.S. in 1927. For a period, he was a research analyst and an investment manager at Sun Life. Later he became the manager of the investment research department at Investor’s Diversified Services (a major mutual fund sponsor) in Minneapolis. Jim wanted Vince to come into Becker and head up the firm’s investment research department. Vince promptly declined Jim’s invitation, but said he could be interested in a more general administrative post, and would assist Jim in hiring someone very well suited to build the firm's investment research services. Jim and his senior colleagues were impressed with Vince’s overall management skills and ideas. He was shortly hired and teamed with Jim promptly to recruit Larry Kahn, as earlier mentioned, to build a research organization centered in the New York office. Both Flett and Kahn became shareholders in 1957.

Vince came into the Chicago office as “administrator without portfolio” and began to analyze the the firm's organizational structure, its key policies and procedures, and, overall, how the firm was being managed. He was in essence an “internal management consultant” and organizational advisor to Jim Becker. Among other things he noted that over 80% of the shareholders were over 65 and thus the firm’s capital was truly “short-term.” He further noted that there was a strong bias in the firm toward “production” with less emphasis on “management.” He noted that there was very little provision and planning to build depth in corporate client relationships and foster retention. He pointed out that salesmen were in many cases hired on the basis of family contacts and friendly associations as opposed to professional sales potential, and that sales training was minimal. He questioned the appropriateness of sales managers being compensated in part on the basis of personal account commissions, and research personnel having unmonitored personal investment accounts. And very fundamentally, he noted that the firm had inadequate planning for management succession.

Talent Infusion

Despite the general organizational deficiencies noted by Vince Flett, Jim Becker, like his father some 35-40 years earlier, had already begun to hire - and push colleagues to hire - and to promote, younger talent. This program was under way in the early 1950s and was continuing later in the decade. In 1950, Roger Brown joined the Chicago sales force and rather quickly became a star producer. His leadership talents and training (Harvard Business School) became obvious and in 1957 he was appointed Assistant Sales Manager under Harry McCosh.

Under Roger’s leadership a sales training manual was created and a sales training program implemented. A number of high quality young men were hired in Chicago including Kenneth Alm, John Mabie, Ken Nelson, Bob Wieczorowski, Bill Osborne, Larry Novac, Neal Breskin, Ernie Janus, Jim Mabie, and Tom McCausland, among others. A similar program was initiated in the New York office and recruits spent some training time in the Chicago office. Dick Driehaus and Dick Elden had their early training at Becker. Somewhat older men like Marine Corps Col. Jim Donoghue were also hired. The new recruits learned from Roger, Harry, and the training program to be good stock pickers, good portfolio thinkers, and excellent salesmen. At the same time, they absorbed practical advice and encouragement and sound investment thinking from the old-timers all around them - Andy Baird, Bill Mabie, Herb Schaffner, Charlie Ritter, and, last but not least, Jim Becker.

In New York, under the guidance of David Dattelbaum (also Harvard Business School), the same early 1950s recruiting was taking place, including Jim Lewis, Burt Weiss, Stephen Weiss, Richard Gilder, and Harold Warendorf, among others. Somewhat earlier, Harry Weber and Everett (Bud) Wallace had joined the firm. Other recruits included George Morris, Howard Berkowitz, Paul Marcus, Steve Grosberg, and Phil Oppenheimer.

Additions to the Chicago Corporate finance department were also initiated in the early 1950s with the hiring of John Stodder and John Colman. They joined Bill Saunders, an experienced “deal man” with extensive contacts in the Pacific Coast timber and paper industry, who was recruited into the firm in 1949. In 1958, John Jachym, with wide-ranging contacts in the professional sports world, was employed. Both men were experienced in originating and completing merger and acquisition transactions. Also in 1958, the author joined the department as a staff associate. In 1960, Ed Jennett, retired Vice-President of the First National Bank of Chicago, also joined.

Commercial Paper Business

In 1956 Bill Eaton retired after 36 years with Becker, having pioneered the firm's distribution of commercial paper in the western region. A year later, Bill passed away and was buried in Vancouver, BC.

In his report to shareholders for 1957, President Becker reported that the firm's commercial paper business had "been handled more or less as a side issue," and that a decision had been made to give this department a "drastic overhaul" with the appointment of John Friedlich (a nephew of James Becker and a grandson of A. G. Becker) as the full-time manager in Chicago. John promptly internally recruited Lewis Glucksman from within the New York Research Department to handle commercial paper in the New York office. In due course, Jack Connor and Jack Donahue joined the Chicago operation.

Jim Becker's decision in 1957 to reinvigorate the traditional central business of the firm – the commercial paper business – was, in a sense, just in time. Whereas in 1939, commercial paper outstandings through dealers hit a high for the 1930s at just over $200 million, and outstandings bumped along during WWII, the level of outstandings began to grow rapidly after the war. They reached some $450 million by 1951 and grew to over $1.9 billion in 1963. It was timely that Becker's participation in this fast-growing market was reenergized.

Exclusive FNMA Notes Distributor

In April 18, 1960, A. G. Becker & Co. achieved a major coup when it was announced that the firm had been selected as the exclusive distributor of the newly devised Short Term Discount Notes of the Federal National Mortgage Association (“FNMA”). The selection of Becker was made, among other considerations, on the basis of competitive proposals. The firm submitted an excellently drafted proposal, principally authored by John Colman, which, coupled with the firm’s extensive distribution network, top reputation, and long experience in and detailed understanding of the operation of the nation’s money markets, won the business. FNMA was chartered by Congress in 1938 to provide a secondary market for mortgages guaranteed by the VA or insured by the FHA. Heretofore, FNMA obtained long-term funding by the public sale of debentures and common stock coupled with the sale of preferred stock to the U.S. Treasury. Short-term funding had been obtained only by borrowing from the U.S. Treasury. The new open-market discount note program provided much greater short funding flexibility for FNMA as well as expanding its access to the broad money markets.

With the exclusive FNMA distributorship, the rejuvenated Chicago, New York, and various satellite operations grew substantially during the 1960s, aided by renewed issuer development, multi-office sales, secondary market service, and highly effective operational support.

As earlier described, David Skall moved to Chicago from Cleveland in 1952 to set up a specialist operation on the newly formed Midwest Stock Exchange. He brought along his son, Malcolm (“Mac”) as part of the business. In January 1961, in a career change, Mac Skall, having moved to San Francisco to set up a specialist operation on the Pacific Coast Stock Exchange, redirected his efforts to the West Coast distribution of money market securities. He quickly became a key member in the firm’s national money market sales network. He promptly gave an especially significant boost to the firm’s early success in distributing FNMA Notes. During the same month in 1961, the Dallas office was opened under Les Frankenthal to strengthen the distribution of money market securities in the southwestern states.

Vince Flett - Continued

In 1954, Dave Stern retired, leaving the office of Chairman open. In early 1956, James Becker completed 35 years of service, as did Henry Getz in April. In June, Howell Murray celebrated 40 years with the firm, and Andy Baird, 35 years. In 1957, Joe Levin, and Maury Cann completed 35 years of service, and Art Curtis and David Dattelbaum, 30 years. In 1958, Herb Schaffner and Harry McCosh completed 40 years of service. In the same year, in his 42nd year with Becker, Howie Murray passed away November 26. Indeed, Vince Flett's observation as to the “short-term nature of the firm’s capital” was becoming a reality.

At the same time, Vince had noted the firm's emphasis on revenue production - particularly in the relatively new stock exchange business. He observed that inadequate attention was being given to the operating systems and the new leadership and technologies that would be required to support the expanding stock commission business. It was clear, too, that needed changes in leadership would impact personnel who had been with the firm for many years.

Despite these challenges, Mr. Becker, with Vince’s support, "bit the bullet" and in 1956 hired Russ Urquart, an experienced back office executive, to come in as Controller and take charge of all Chicago and New York back office operations, and the related forward planning. Very soon, in 1961, a major portion of Becker's back office operations and bookkeeping were transferred to the Midwest Stock Exchange Service Corporation, which transfer continued well into 1962. By that date, Russ had the assistance of Fred Carboni of New York, Joe Goeschl, who had moved to New York from Chicago, and Ralph Coffey and Jerry Beebe in Chicago.

The decision by Jim Becker, catalyzed by Vince Flett, to beef up the accounting and operations management of the firm was similar to that of his father in hiring Lester Roth - an excellent back office is a vital part of an excellent financial services firm. (Note Appendix-8 once again)

Younger Key Personnel Advanced

In 1958, John Stodder, John Friedlich, and Harry Weber were elected Vice Presidents. These elections were followed in January 1960 by the election to Vice President of John C. Colman, John Fitch, Lewis Glucksman, Milton F. Lewis, Everett (Bud) Wallace, and Stanley Winter, and the election of Joe Levin to Executive Vice President.

Investment Research

With the assistance of Vince Flett, as promised, Lawrence Kahn was hired in the New York Office in 1954 as Vice President and Director of Investment Research, filling a vacancy of some years. Larry inherited two excellent analysts in Chicago (Stan Winter and Gus Torrey), hired Frank Kiser (Chicago), and then promptly built the New York office research roster to include Jane Brett (returning), Bill Earle, Claude Wilson, John Holschuh, Myron Baker, and Robert Wilson (who later became a broker and then left Becker to became a prominent independent investor).

Langum Dinners

It was also during this period that the firm began to hold "John Langum Dinners" in various cities throughout the nation. John was an independent economic consultant on retainer to the firm (following the pattern set by David Friday many years earlier). John Langum closely followed national economic data, opinion, and trends and wrapped them together to present, at each dinner meeting, a comprehensive view and forecast of the national economy. John was informative and entertaining. Langum dinners were presented periodically in a number of major U.S. cities. Through this periodic enlightenment, John extended the firm's reputation for thoughtful and valuable financial and economic insights to investment and corporate finance officers who were existing or potential clients.

New York Office Changes

In the New York office, James P. Lewis joined the firm in 1958 to assist Dave Dattelbaum in sales management and the New York office’s underwriting syndication work. In 1959, Jim was appointed Assistant Sales Manager, formalizing his support of Dave. He was also to give assistance to Harry Weber in organizing a systematic institutional sales effort. In late 1961, his syndicate activities were taken over by Frank Lockwood, who joined the firm as National Syndicate Manager. This position initiated the formal transfer of the firm's national central underwriting syndication function from the Chicago office (Andy Baird and Art Curtis went to the New York office).

In December 1955, with organizational growth now well under way, Becker moved its New York operations to offices in 60 Broadway, ending almost 30 years of occupancy of its own building at 54 Pine Street. Operations in this location were short-lived with a move, in mid-1962, to much larger and more modern quarters at the new 60 Broad Street building.

Corporate Finance Transitions

The firm's corporate finance business serving established and new clients advanced during this period primarily through the efforts of the firm's seniors – Becker, Sherman, Johnston, Getz, Levin, Baird, Mabie, and Murray (the latter until his death in 1958). However, a younger staff was developing in Chicago, including John Stodder, John Colman, Bill Saunders, John Jachym, Paul Judy, John Griner, and Warner Rosenthal, joined in late 1960 by Kingman Douglass. Unfortunately, John Stodder left the firm as of Dec. 31, 1961. During this period, there was a steady leadership transition in the Chicago corporate finance department, from Levin, to Getz, to Saunders, to Colman.

Management and Board Succession

The 1958-60 promotions of a cadre of younger men to Vice President, and of Joe Levin to Executive Vice President, were beginning to unveil the influence and advice of Vince Flett. On the subject of succession planning and action, a major move came in the summer of 1961, with the election of William Mabie as President, Irving Sherman as Vice-Chairman, and Joe Levin to the added title of Chairman of the Executive Committee - all announced by James Becker in June 1961. With these moves, Mr. Becker continued as Chief Executive Officer but also was elected Chairman of the Board, filling the vacancy created with Dave Stern’s retirement in 1954. All parties were reminded of this vacancy with Mr. Stern’s death in mid-1959. These top management moves established a senior executive team for an interim period in the event of James Becker’s untimely death.

In 1958, the Board of Directors had settled down to eight persons – Becker, Baird, Getz, Levin, Johnston, Sherman, and Murray, joined in midyear by Flett. In December 1961, continuing the management transition program, Roger Brown, John Colman, John Friedlich, and Harry Weber were added to the Board. Unfortunately, no photo of this Board exists in the archives.

Enhanced Internal Communications

Starting either in or before 1956, internally, the firm began to periodically distribute a legal-sized newsletter, the "A. G. Becker & Co. Bulletin." (Later called "BeckerBriefs" and "GroupDynamics.") The document was published in Chicago but delivered overnight to New York and to all other offices. This document reported:

- Personnel news (new, retiring, resigning employees; managerial promotions and elections as directors and shareholders; department transfers and changes in assignments; organizational structure changes; and similar items to inform all hands)

- The Offering Calendar (a listing, by future date, of all underwritings, managed or participational, in which the firm had purchasing commitments). This information was primarily for the retail and institutional sales force. In the early days of the calendar, there was a code next to each offering from which it could be determined what percentage of the sales price would be available to the salesman as a commission.

- Recent Financial News of Selected Companies (in particular, a summary of quarterly and annual revenue and earnings releases of client companies and other companies headquartered in or near Chicago, and in some cases, New York, in which Becker had a special interest. Included were some companies for which AGB was a primary over-the-counter market maker in their shares.)

External Communications

As described in Appendix-5, the firm’s advertising during the post-war period was pretty mundane. Some special formats were tried and dropped; firm personnel probably used the word “ugly” to describe them. However, this period was the precursor to a fabulous advertising program starting in 1965, as is covered in Appendix-5. And thereafter the firm's overall external communications program became particularly active and effective.

Organizational Growth

The firm closed 1961 with 470 employees, up from 275 at the end of 1955 (an increase of 70%), and up from 416 and 390 respectively at the end of 1960 and 1959. These personnel counts imply a net employment growth rate (additions less resignations, retirements, and dismissals) over this period of about 9% per annum. With this growth in personnel came the inevitable need for more office space as earlier reported.

Offices

By the end of 1945, as noted earlier, the firm had reduced its offices to Chicago, New York, and Milwaukee. San Francisco was “reopened” in early 1946 by Carl W. Stern for a short period of time and then again (or perhaps a continuation) in 1958 by Malcolm Skall, for a sustained presence in the city. Carl Stern, an attorney, was a son of David Stern and grand-nephew of A. G. Becker. Satellite offices to Chicago were opened in Rockford under Jack L'Hommedieu (1952) and in Roseland under Alwin Pearson (late 1953). In 1950, an office was opened in Albany, under Russell (Buck) Boyd, and in Indianapolis, first under Walt Stuhldreher and later under Oliver Maggard.

In summary, as of the end of 1961, the firm had offices in Chicago, New York, San Francisco, Albany, Milwaukee, Rockford, Indianapolis, and Roseland - no change since 1955.

Financials

Key financial information for A. G. Becker & Co. and its successor firms from 1956 to 1984 is compiled in this record. The following is a commentary for the sub-periods within the overall 1947-61 period.

On becoming a NYSE member, the combination of the AGB Partnership and the Corporation as of October 24, 1947, showed a net worth of $2.4 million. Moving ahead four years, to July 31, 1951, the net worth of the business had increased to about $2.6 million.

Moving forward another six and a half years, to December 31, 1957, the company's net worth had grown to a little over $3.3 million, up about $700 thousand for the period.

Prior to 1957, as far as can be determined, the Chairman reviewed the firm’s financial progress for the prior year at a shareholder’s meeting held shortly after the fiscal year end (December 31). Starting in early 1958, James Becker initiated a written shareholder report distributed to all shareholders highlighting not only the financial condition and results of operations of the firm for the year just completed, but also summarizing key personnel changes.

This new practice was undoubtedly followed again in early 1959-1961, but the archives do not contain those reports. The report covering 1961, as issued in early 1962, is available in the archives. This report nicely augments the above references to key activities in 1961 and goes on to record that Becker's net worth had by this time expanded to $7.3 million, up some $4 million in the five-year period, of which about $1.5 million was retained earnings (earned mostly in 1960 and 1961), and the balance new capital. (1)

A major initiative was undertaken during 1961 involving the transfer of ownership from older to younger employees. New capital in the amount of $778,000 was raised during 1961 in cash or by installment payments due over the next four years. The firm realized net income of just under $1.2 million on total revenues of $10.4 million. Net asset value per common share reached $18.93 as of December 31, 1961, over double the $9.31 value as of December 31, 1956. (Adjusted for many subsequent stock splits and stock dividends, respectively $.85 and $.41.)

Shareownership

Coming out of World War II, and after reorganizing the firm's ownership, A. G. Becker & Co. was owned by fourteen employees in 1947. By the end of 1961, this group had expanded to 24.

The expansion of share ownership in the firm was a key objective of Jim Becker, and strongly encouraged by his internal consultant, Vince Flett. As early as the late 1950s, Jim personally established with the firm’s principal bank, First National of Chicago, a stock purchase financing plan under which a shareholder invitee could put down in cash 25% of the aggregate price for the purchase of Becker shares and obtain from the bank a personal installment loan for the balance. The loans were for a term of ten years, at a reasonable interest rate, with the principal and interest payable monthly deducted from the employee’s paycheck, and then forwarded to the bank. The firm did not guarantee these loans, but did agree with the Bank to monitor and administer them, and in the event the employee left the firm or otherwise didn’t pay his/her loan, the shares would be redeemed and the loan balance repaid, with only the residual turned over to the former employee.

******************************

(1) For those who wish to read the annual reports of the firm for the fiscal years 1957 forward to 1983 (except for years in which the archives to not contain a report), including reports that were issued internally only to employee-shareholders and then later to the public, all these reports are available in chronological order in Annual Publications. To make it easier for all readers to survey the record of key financial data for the firm from 1957 to 1984, the author has compiled this data in this exhibit.