Honeymoon – 1975 to 1977

Honeymoon – 1975 to 1977

Developments in 1975-1976

Market conditions in 1975 and 1976 were generally favorable for the various businesses of BWP, despite the turmoil in the equity markets by reason of negotiated rates which were put into effect in May, 1975. The stock market was up some 50% in the first half of 1975 and volume up 40%. Short term interest rates were down 300 basis points for the year. 1976 showed continuing disruption in the equity markets, but good conditions existed for fixed income and corporate finance operations.

As noted earlier, the Agreement of Amalgamation was signed in July, 1974, and by September the predecessor's corporate finance division was incorporated within Warburg Paribas Becker Inc. ("WPB"). By year end, the Credit Securities Group continued forward under the predecessor name, A.G. Becker & Co. ("AGB"). The balance of the organization was grouped under the banner of Becker Securities Corporation ("BSC"). Jack Wing became President and head of BSC, with Fred Moss as Chairman; Jack Donahue became President of AGB.

Although it is unclear in the archives, the author presumably became interim President of WPB until late 1975, when Edward Dugan joined WPB as President, succeeding the author, who had been Chairman and interim COO. Ed had served fourteen years in the investment banking department of Smith, Barney where he rose from trainee to coordinator of the firm's new business program and business developer with large corporations. He also had venture capital and international finance experience. He was a Director of Smith, Barney for the last seven years.

In April, 1976, Rudolph (Rudy) Peterson, formerly Chairman of the Bank of America, joined BWP as a Director, and WPB as Co-Chairman with the author serving as the other Co-Chairman.

Warburg Paribas Becker, Inc. (WPB)

WPB's activities in the balance of 1974, and 1975-76, were quite favorable. Managed or co-managed offerings were up in 1975 by 44% and then in 1976 by 50%. Specialized financing, private placement, and merger and acquisition capabilities for independent finance, captive finance, and bank holding companies, and banks themselves, along with lease financing and Title XI ship financing, continued strong, with many new client relationships developed in the process. During 1976, WPB moved into corporate real estate financing and, with the expertise of Bill Pope, took a leading role in Export-Import Bank guaranteed debt financing, including a $367 million co-managed financing for the National Power Corp. (Philippines). In 1976, WPB served some European interests in acquisitions in the U.S., services that would not likely have come to WPB except for the Warburg and Paribas relationships.

In early 1976, the firm welcomed Charles (Soapy) Symington, as senior Syndicate Manager with good securities firm experience and industry connections. With Lon Moelentine's assistance, Charlie was kept busy with the high growth of WPB's originations, and with handling some 445 underwriting participations during his first year. Once again, too, Becker’s distribution capabilities were outstanding.

In May, 1976, the firm followed the path of many Wall Street and London firms by adopting the title "managing director" for senior professionals involved in investment banking work.

Organizations which we were pleased to serve in an investment banking capacity in the 1975-76 period included: the European Coal and Steel Community; National Power Corp. (Philippines); AMP; Amtrak; First Chicago Corp.; Colt Industries; Cyprus Mines; Clark Equipment Credit; Cargill; Aetna Business Credit; Diamond M; Gambles Credit; Hallmark; Hayes-Albion; IOT Corp.; International Minerals; Mack Trucks; Pierrefitte-Abbey; Standard Oil of California; Jim Walter; Wells Fargo Leasing; American Credit; FMC Finance; Fraser Companies; General Telephone of Ohio; Trans Union Leasing; Pacific Far East Lines; Crowley Marine; Kentucky Utilities; Capital Financial; Marriott; Marine Leasing; Cone Mills; Continental Grain; Southwestern Investment; GATX Leasing; El Paso Electric; National Can; Mississippi Chemical; Saga Corp.; Hawker Siddeley; Duncan Electric; and Societe des Ciments Francais.

A.G. Becker & Co., Inc. (AGB)

During 1976 and 1977, AGB's money market prowess was at its best. Some $150 billion in the short term notes of high credit corporations, major banks and their holding companies were purchased and sold over the two year period. In 1975, the firm formalized a commercial paper issuer development program initiated in the late 1960s by Ray Ryan, then assisted by Claude Wilson, developed more systematically by Dick Frodsham , moved forward more intensively and comprehensively by Roger Vasey, and succeeded by Jim Ledinsky. In 1976, the firm experienced a net increase in top-rated issuers greater than the aggregate increase of all other dealers.

In 1976, the firm began to deal in Eurodollar CDs in the London office. Rather promptly, as best could be determined, Becker became the leader in that market, under Jack Cunningham. Even when Jack left Becker in 1980, the business continued to prosper under Ed Voelker.

Founded on the basis of statistics internally developed by the WPB-AGB credit group, AGB and WPB, in 1976, introduced BANKDATA. This service encompassed comprehensive, regularly updated, fundamental credit data on the top 100 US banks. The service was of keen value to CD investors and was subscribed to rather extensively.

In this two year period, the firm's leadership as a dealer in U.S. government and agency paper was extended, particularly in the relatively new GNMA securities, of which the firm managed or co-managed some $2 billion in 1976. In that year, the firm joined the IMM and took a leading role in dealing in treasury bills futures. In the same year, the firm passed its fifth anniversary as a primary reporting dealer and was increasingly being depended on by the New Yord Federal Reserve Bank Open Market Desk for its money market feel and analysis.

In corporate taxable bonds, the firm excelled with underwriting participations in these instruments, up some 20% in the two year period. During 1975, the firm began to offer the "Corporate Bond Service," an online, computerbased service to institutional bond traders to assist them in quick credit and security research and market valuations. This service was met with positive acclaim and use.

AGB also distributed some $8 billion in Municipal Notes in 1975. Managed or co-managed tax-exempt bond underwritings were up 44% and then 100% for the two year period. The firm successfully entered the field of funding health and educational facilities.

Finally, AGB successfully opened a Houston office, managed by Jack Harrington, who moved from Boston. The office and manager were well received in Houston's financial community.

Becker Securities Corporation (BSC)

The various activities within BSC for the two year period had mixed challenges and results. As noted earlier, stock market prices and volume were up substantially in the latter half of 1975. The high volume continued in 1976, but with high levels of competition especially in the institutional markets, negotiated rates took down margins. More institutions wanted to deal as principal and the firm, after many years of block positioning, was able to respond to this need and designated more capital for these accomodations. During 1975, BSC was handling five to six block crosses each day. Transactions in the sale of corporate underwritings, both managed and participative, were up 49% in 1976. The LA office came on stream with 13 salesmen, which helped the business.

Investment Research

The output of the investment research department continued to be of high quality, under Stu Porter's leadership. The April, 1975 Wall Street Journal article boosted the recogniton and reputation of Becker's investment research. A February 20, 1976 PMA seminar in Longboat Key, Florida attracted 450 subscribers, two times the 1975 attendance.

Funds Evaluation

The Funds Evaluation Services, now with 13 flavors, continued to grow during this two year period, but with many challenges. The passage of ERISA in 1975 gave a boost to the business, but May Day had an offsetting and perhaps greater impact. The Group finished 1975 with some 1,400 sponsored fund clients, and some 200 portfolio manager clients for the Institutional Funds Manager product. A bond portfolio performance evaluation service was introduced and well received. However, with negotiated commissions narrowing, especially in the institutional business, and with the battle between executions and research going strong, and principal trades thrown in requiring capital and risk, obtaining payments for providing funds evaluation services out of dwindling commissions was not easy. Furthermore, a rule was put in on the exchanges which prohibited broker A from giving up some of its commissions to Broker B at the direction of the client - a practice which beforehand was quite helpful to receiving commission payments for funds evaluation services.

On the other hand, it was quite clear that pension fund trustees could pay BSC cash for its valuable portfolio evaluation services, particularly now, after many years of proof as to the value of Becker’s analyses to the trustees in their fiduciary function. And thus the movement to cash fees was initiated and as of the end of 1976 was almost complete.

Maintaining a steady product innovation pattern, in 1976, the Funds Department developed a Compendium of Investment Managers, a publication of wide interest to all kinds of funds sponsors. A Management Search Service was scheduled for introduction in 1977. Further, it was announced that BSC, partnering with a major bank, was developing a system which would operate an index fund, which system would soon be offered to institutional clients.

By this time, BSC's funds evaluation services were well established in Canada due to the early work by George Baxter, travelling from the New York office. This was followed by the excellent continuation and expansion of clients by Harty McKeown working out of the Toronto office which was established in 1975. Over half of the major Canadian corporations were on the service by this time. In 1976, the transition from commissions to cash in Canada was accelerated by the passage of a law or regulation requiring or encouraging cash to be used for such services.

Organizationally, by 1975-6, the Funds Evaluation Department, reached real maturity and cohesiveness, and had established a high standard of profesionalism and a unique culture. About that time, in a national meeting of the department. Bob Brehm took a number of photos which he organized into an attactive montage.

{kind=link}

Dealer Services

In the investment dealer business, the traditional practices of many clients were disrupted by May Day and the effects carried forward from mid-1975 well into 1977. BSC offered completely unbundled services so dealer clients could use any portion of the array they chose: financing; clearing-disclosed; clearing-non-disclosed; execution; principal trading; or three levels of research. This flexibility and good service kept most of the firm's 250 clients on the books. Approximately $9.2 billion of orders were handled by this group in 1976. BSC's floor broker representation on all exchanges (NYSE 12, ASE 5; MSE 6; CBOE 11; and PCSE and BPW 1 each), coupled with four geographicly dispersed, upstairs order desks, all tied in with an expensive but exotic and highly effective communications system, continued to be central to the firm's order handling services, ready to deal as agent or principal. This client option had been prepared in earlier years.

Activity on the relatively new CBOE continued to grow, followed by the intiation of options trading on the American and Baltimore-Philadelphia Exchanges. Institutional use of options was growing as legal barriers were being removed. By the end of 1976, BSC had some 175 employees rather directly involved in various aspects of the firm's overall options business that was being conducted on three exchanges.

BSC's specialist clearing services continued to expand. For example, by late 1976 BSC operations were clearing the trades of ASE stock specialists handling some 35% of the exchange's listed issues, and some 33% of its options issues. The firm's ASE clients included three out of the five most active specialists.

Equity Trading

BSC's equity trading results were satisfactory for 1975, including the specialist operations on the MSE, AMEX, and PCSE. Proprietary trading was also favorable. Results in this area for 1976 were nondescript.

Sales Management

In key management changes, Ed Schiewe moved into sales management as head of General Accounts in Chicago, and Bob Rafford similarly in New York, succeeding Clarke Young. In Chicago, John Rogers took on Major Institutional Sales. Later, during 1976, Burt Weiss retired after many years of service going back to 1954 when he joined Becker. John Levy, now Senior Vice President, took over national management of General Accounts, Institutional Sales and Research. Bill Smith became manager of Correspondent and Execution Services.

Private Investments

In the private investment area, BCA continued to make clear advances as a special and knowledgeable source of financing of cable systems and other communications operations. By 1975, BCA had committed some $38 million to client companies since its intiation in 1973. BTA, originated in 1968, was in the process of liquidation as 1976 ended, with a good investment gain for investors over the period. See Appendix-6 for more details.

Operations

Operations support of both equity and fixed income activities was maintained in BSC overall under Ray Holland, with Line Operations under Joe Goeschl and Staff Operations under Ben Witt. A new, very large IBM computer was successfully installed in Chicago.

Adminstration

Administrative Services continued under Bob Vance, reporting to Jack Wing. The name of BeckerBriefs, the BWP internal newletter, was changed to GroupDynamics in April, 1975. The Guide to Publicly Owned Corporations in the Chicago Area - some 290 corporations - continued to be widely popular. Accounting, Control, and Planning was under Tom Matchett; Comunications under Dave Scholl; Personnel under Jim Toner and Karen Canty; Office Services under Russ Mayer and Ed Russin; and Telecommunications under Joe Mills. The Communications Department was responsible for writing, designing, and printing product and promotional brochures, at the request of marketing managers, and with the firm's breadth of services, this activity was now extensive.

Overall

In the publicly distributed 1975 Annual Report, the President (the author) noted that "the benefits of diversified capabilities, appropriate controls, and the ability to capitalize on emerging opportunities" would continue to be important to BWP. A year later, in the activities section of the 1976 Annual Report, the President noted that success in the securities business depended on "building interrelated teams of professionals with demonstrated intellectual capacity and motivation." Thus, at least from the point of view of the BWP management and employee shareholders, the first two plus years of affiliation with Paribas and Warburg appeared to be working well. BWP was moving forward during good (and despite bad) markets just as would have been done by the old AGB, if not better, and innovative services and capabilities were being added on all fronts.

Organizational Growth

Total employment grew from some 1,600, at the end of Fiscal 1974, to 2,166 at Fiscal 1976 year end, up some 35% for the two year period. At the end of Fiscal 1976, there were 205 employee shareholders. The assets of the two profit sharing Funds reached over $17 million as of Fiscal year end 1976, taking into account the 1976 contributions. At that date, 1095 employees are beneficiaries of these funds including 307 who were first time participants in 1976.

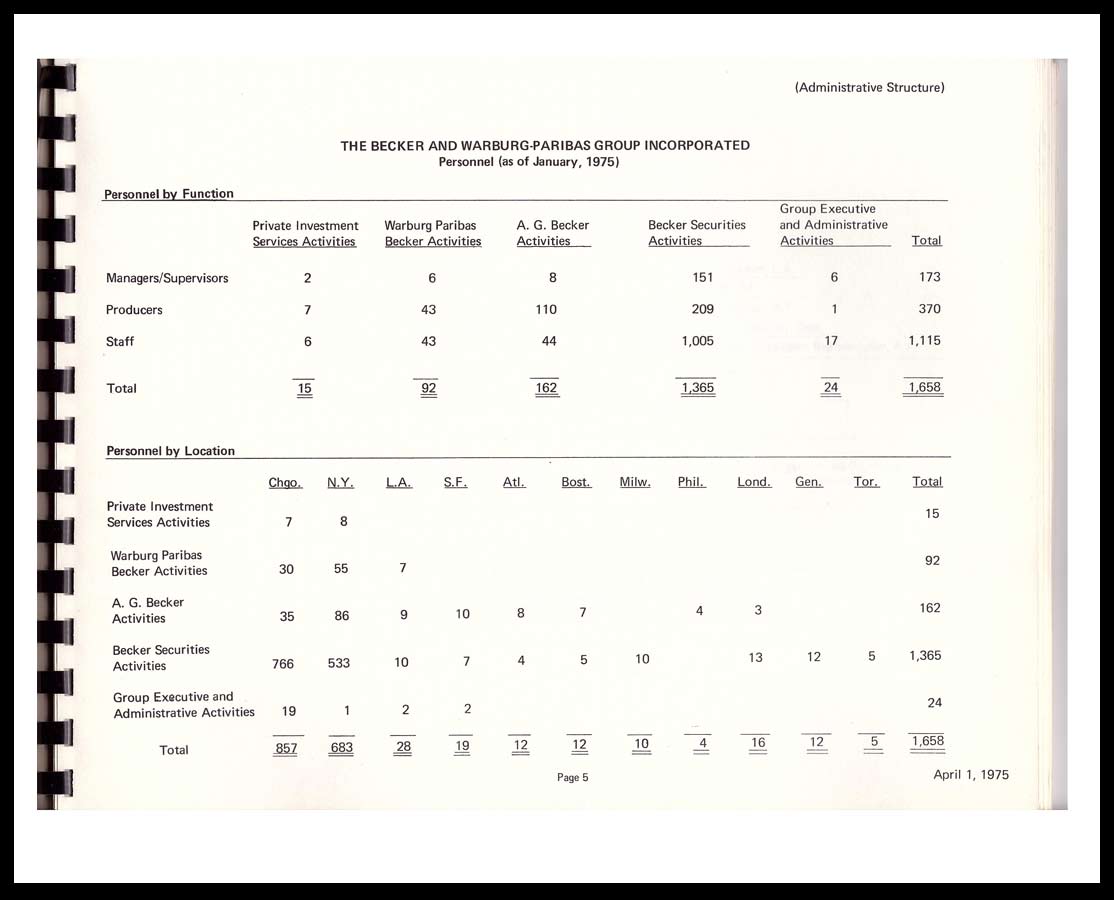

A good sense of the growth and structure of the organization during this period can be drawn from tables which were published to all shareholders during this period. The status as of early 1975 was as shown here and in July 1977 as shown here.

{kind=link}

{kind=link}

The Becker Pension Fund ended Fiscal 1976 with just under $10 million. There were 50 pensioners at the end of Fiscal 1976 receiving $14,200 in distributions per month.

Offices

As of the end of 1975, BWP offices were located in Chicago, New York, Los Angeles, San Francisco, Atlanta, Boston, Geneva, Houston, London, Milwaukee, Philadelphia, and Toronto.

Financials

As can be seen in the long-term summary of key financial data, BWP's revenues reached $137 million in Fiscal 1975 and were essentially the same for Fiscal 1976. Operating Income and Net Income were also about the same in these two years respectively in the $14-15 million and $7-7 1/2 million ranges. Stockholders' Equity grew from $27 ½ million at the end of 1974 to just short of $42 million as of Fiscal 1976 year end. During the same period, capital funds grew from $56 to $66 million. Net asset value per Class A and B share as of October 29, 1976 rose to $31.89 up by a little over 40% as compared to $21.22, the value per share used in the 1974 Amalgamation process. (Adjusted for a subsequent stock split and a 10% stock dividend, the amounts were $14.50 and $9.65 respectively).

Developments in 1977

The archives unfortunately are meager with respect to developments in fiscal year 1977. The following summary has been pieced together from available materials.

Overall

Firstly, whereas conditions for BWP's business mix were relatively favorable for 1975 and 1976, the first full two years after the amalgamation, they generally were reversed for 1977. Price compettion to handle equity trades increased on sluggish volume and declining equity values. Even though WPB's managed or co-managed business was up, corporate underwritings and participations overall were generally down.

Becker Securities Corporation (BSC)

In BSC, the emphasis on thinking more about "portfolio composition" than about "individual stock selection" was being carried forward in the general accounts sales force. More training was provided on how bonds fit into more portfolios, and how to assemble that asset class in a portfolio. Given the growing emphasis on principal vs. agency transactions, the over-the-counter operation was re-expanded and new capital allocated to this department. Funds evaluation services continued to grow as did clearance services to market makers of all sorts.

Jack Wing and Fred Moss continued their overall management of BSC, including brokerage services under John Levy; Funds Evaluation under Stu Gassel; Executions Services under Ken Nelson; and Operations under Ray Holland. Toward year end, Barry Haase left the position of General Counsel to become the manager of the Dealer Services. He was succeeded as General Counsel by Randy Harris.

Into 1977, Operations support for BSC’s general securities was placed under Ben Witt, reporting to Ray Holland, and supported by Kevin Young(NY), Dick Cooper(Chicago), and Ray Lownes(LA), while support of the AGB credit securities operations was being managed by Joe Goeschl and Tom Matchett, both in New York. Accounting Central & Planning were centered in Chicago under Steve Stock, Tom Evey, and Zinaida Strods.

A.G. Becker &Co., Inc. (AGB)

The distribution and market making of the full range of fixed income securities by AGB continued to advance despite the rise in interest rates, all under Jack Donahue's and Tom York's oversight. Sales leaders like Al Hanley and salesmen like Walt Noonan, Bill Breen, and John Patti (Chicago) as well as Doug Robbins and Bill Mullhern (New York) contributed to this success. AGB' s Eurodollar business in London under Jack Cunningham was booming. A Credit Securities office was opened in San Juan and given limited authority to underwrite and distribute the securities of Puerto Rican issuers. Jim Ledinsky succeeded Roger Vasey as head of the Commercial Paper Issuance Development Program.

An AGB office was opened in Cleveland in late December and with this move, the Chicago and New York money market and bond sales were being substantially augmented by a powerful group of sales leaders in seven branch offices, as follows: Atlanta (Russ Wigh); Boston (Dan Hogan); Cleveland (Skip Fleming); Houston (John Harrington); Los Angeles (Steve Kirch); Philadelphia (John Canzanella); and San Francisco (Jay Kellett).

Warburg Paribas Becker, Inc. (WPB)

Managed and comanaged underwritings and the private placement of debt and preferred stock by WPB continued to grow at a high rate. By year end, WPB was centrally involved in the distribution of over $3.5 billion in securities. Merger and acquisition activity was also brisk.

WPB management under Ed Dugan consisted of Dan Good (Central and Western) backed by Bob Henkle and Bob Karlblom; Barry Friedberg (Eastern) backed up by Bob Nau, Howard Sodakoff, and Milt Walters, with Sangwoo Ahn (Southwest); Karl Hermann (International), and Laurent Michel (Business Combinations). Dan Good was also overseeing Dick Kavanagh in Chicago Municipal Finance.

During 1977, investment banking services were provided to a range of old and new clients but the archives are inadequate to reporting these old and new relationships.

The Becker and Warburg-Paribas Group, Inc. (BWP)

The Treasury and Financial Planning operations of the firm were now grouped under Bill Cockrum's oversight along with the Credit Department and Private Investment Services.

In July, 1977, Finance Magazine listed BWP, with $66 million, as fifteenth largest in capital funds in the US securities industry. Interestingly, there were ten firms in the top twenty which had capital between $60-80 million. Goldman Sachs was seventh in the list at that time with $95 million.

Early in the year, BWP completed a housekeeping project which had been in the making for some time - i.e., a statement of policy as to the criteria for officer elections. The criteria were adopted by the Executive Committee which also established for the first time various titles for supervisory and junior staff personnel - titles which included Operations, Accounting, Systems, and Administrative Officers.

Decision To Step Down

Of special consequence to the author and to the organization as a whole was his decision to "step down" as President and CEO, which announcement was made in early April. He advised the Board of Directors that it was his goal to relinquish this office within the next 12-24 months. He expressed the thought that by year end he would have been in his position for some 10 years and it was time for another person to take the helm and "guide the next stage of BWP's development." He indicated that he intended to remain a shareholder and engage in investment banking work. He also indicated that he wished to expand his community and civic activities, and to pursue certain personal interests for which heretofore he did not have the time.

The author put forth his ideas to representatives of Warburg and Paribas as to possible internal successors. There was no support for these recommendations as none of the people put forth was an “investment banker.” This author’s decision was unexpected by the Board including both resident and non-resident members.

New Committees

The Board promptly established a Search Committee composed of key management (other than the author) and representatives of Warburg and Paribas, and began to assemble names. By unanimous consent of all members, the Committee was chaired by Ira Wender.

Shortly thereafter, and partly in connection therewith, the Board decided to expand the Executive Committee by adding Bill Cockrum and Geoffrey Elliott (a Warburgian now in New York), joining the existing members who were Paul Judy (Chairman), Jack Donahue, Jack Wing, Fred Moss, Ed Dugan, Pierre Haas, and Ira Wender.

The Board also decided to set up two other standing Committees, as follows:

Policy Committee (Rudy Peterson(Chair), Geoffrey Seligman, Pierre Moussa, and Paul Judy).

Audit Committee (Malcolm Skall (Chair), Bill Cockrum, Ira Wender.

In addition, the Board decided to set up (or to continue) the following sub-committees of the Executive Committee. Various managers as well as Board members were appointed to each.

- Operations and Personnel (new)

- Planning and Development (new)

- Financial Management (succeeding the Banking Committee)

- Computer Systems Planning

- Commercial Paper Credit Review

- Dealer and Market Maker Review

- Internal Audit and Compliance

- Corporate Underwriting Review (succeeding Equity/Debt and Pricing in each case)

- Municipal Underwriting (succeeding Managed and Participating U/W Review)

- Investment (continued)

- Investment Valuation (continued)

Search Committee Work

Over the summer and into the late fall of 1977, the Committee began to have contact with and query a variety of candidates, and to interview some. Since the author was not privy to exactly how the Committee functioned, and there being no records, information is scarce as to the possible candidates considered and whether interviews were held. Some of the candidates included names that the author had considered a few years earlier in the process of filling the position of operating head of WPB. The author had interviewed some of those candidates.

During the period from mid-1977 to year end, the Board also considered a possible merger with another firm with the advantage, among others, of obtaining new central leadership. Rather intensive discussions were held with the key partners of Kuhn, Loeb ("KL"), but after one session, it was decided rather quickly, and generally mutually, not to pursue the matter. There may have been other possible mergers considered at this time by the Search Committee, or by the Board itself (with Paul Judy recused). However, to the author's knowledge, there were no merger discussions at this time except with KL.

During 1977, the Committee reportedly considered a number of candidates for the Group CEO position, interviewed some, and discussed rather intensively what was wanted in the person filling this position. Toward the end of 1977, the employee members on the Search Committee joined those from Warburg and Paribas in proposing that Ira Wender be selected to succeed the author as President.

Board Elections and Announcements

On January 18, 1978, the Board of Directors elected Ira Wender as President and Chief Executive Officer, and Chairman of the Executive Committee. In this meeting the author expressed his disagreement with the expected vote, expressed serious doubts as to Ira's capabilities for the CEO role, gave his reasons, and requested that the minutes show his negative vote. The Board was, however, unanimous in the selection, except for the author's vote.

At the same meeting, John Donahue and Jack Wing were elected Executive Vice Presidents of BWP. These elections were effective on February 1, 1978. In addition, Michel Francois-Poncet (Paribas) was added to the Board.

A public and internal announcement was promptly made of these elections. In November, 1977, Pierre Haas and David Scholey replaced Pierre Moussa and Geoffrey Seligman as Co-Chairs of the BWP Board of Directors. Thus, an advertisement of the new BWP leadership was made in the national press on January 18, 1978, including the author being elected Co-Chairman of WPB.

Financials

For the 1977 fiscal year ending October 28, 1977, BWP published a brief (two page), unsigned, public Annual Report. The report was probably unsigned due to some confusion in the top management transition taking place in January, 1978. The report summarized the revenues and net income for 1977 but did not include a complete Statement of Operating Results for the most recent two years, as had been the prior practice. A Statement of Financial Condition was included, along with the listing of the Board of Directors (as above reported), and the firm's office locations as of the end of 1977.

The archives do not have an internal report to shareholders for Fiscal 1977. It appears that no such report was prepared. The following information was therefore collected from 1978 reports and the brief 1977 public Annual Report.

Revenues for Fiscal 1977 declined to $120 million down from $137 million for 1976. Expenses were about level. Thus operating income before taxes dropped from $14 million to $1 million. After tax income was $937,000. Total assets and liabilities increased from a little over $1.4 billion to well over $1.6 billion. Capital funds edged up slightly from $66 to $67 million while stockholders' equity was maintained at about $42 million.

Net asset value per share on October 28, 1977 was $28.52 versus $28.99 a year earlier, for Class A and B shares. It was $26.11 for Class C shares. (Adjusted for a subsequent stock split, respectively, $14.26, $14.50 and $13.06).

Industry Developments

In late November, 1977, the merger of Lehman and Kuhn Loeb was announced, as the latest “in a trend . . . in the financial community.” Other consolidations mentioned as having taken place over the past few years were Reynolds and Dean Witter; Loeb Rhoades and Hornblower Weeks, Noyes and Trask; Mitchell Hutchins and Paine Webber; Faulkner Dawkins and Shearson Hayden Stone. It was noted that the Lehman KL merger would result in a company with 1,700 employees in seven offices and with capital of some $80 million.